In the final quarter of FY 2024–25, several listed manufacturing companies began preparing their annual reports only to discover that compiling ESG data was far more complicated than expected.

Energy consumption numbers from factories did not match sustainability dashboards. Waste management records from vendors were incomplete. In some cases, HR departments could not verify diversity statistics used in earlier sustainability reports.

What many companies assumed would be a simple disclosure exercise quickly turned into a compliance challenge.

BRSR reporting has fundamentally changed how Indian listed companies disclose sustainability performance. The framework requires structured, numerical, and auditable ESG disclosures across environmental, social, and governance indicators.

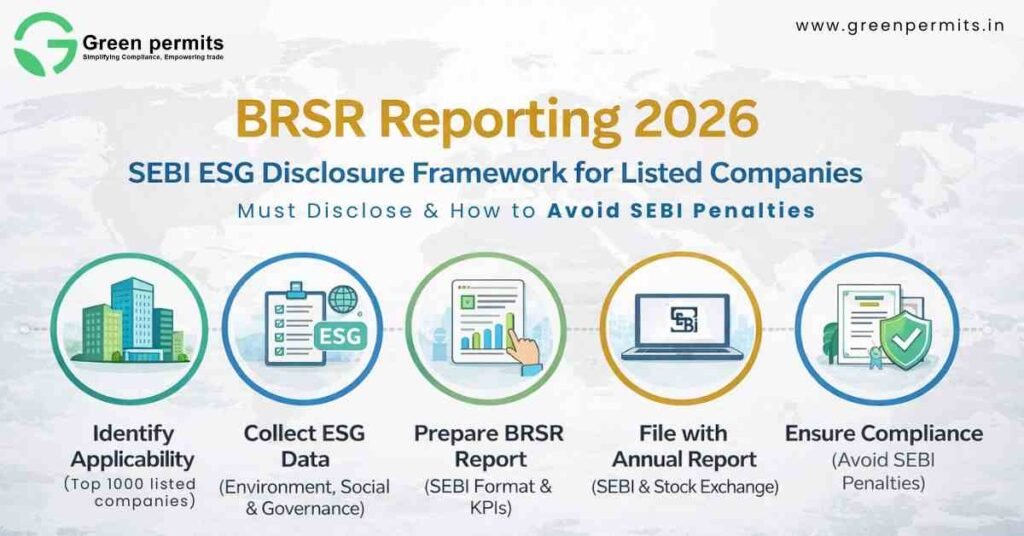

For the top 1,000 listed companies in India, BRSR reporting is now a regulatory requirement linked to SEBI listing compliance. Incorrect disclosures can result in exchange queries, reputational risks, and investor scrutiny.

Understanding what must be reported in 2026 is therefore critical for corporate compliance teams, ESG managers, and board-level governance committees.

Business Responsibility and Sustainability Reporting (BRSR) is India’s structured ESG disclosure framework introduced by the Securities and Exchange Board of India to enhance transparency in corporate sustainability practices.

The framework replaced the earlier Business Responsibility Report (BRR) and significantly expanded the scope of disclosures required from listed entities.

Under BRSR, companies must report quantifiable sustainability data across environmental performance, employee welfare, supply chain practices, governance structures, and ethical business conduct.

The reporting structure is aligned with the National Guidelines on Responsible Business Conduct (NGRBC) which outline 9 sustainability principles governing responsible corporate behavior.

The BRSR framework became mandatory starting from Financial Year 2022–23 for the top 1,000 listed companies by market capitalization.

Key features of BRSR reporting include:

Typical ESG indicators reported in BRSR filings include:

Large listed manufacturing companies often report environmental metrics such as:

These disclosures provide investors with measurable insights into corporate sustainability performance.

BRSR reporting operates within India’s broader corporate governance and sustainability disclosure ecosystem.

The framework is enforced through SEBI’s listing regulations and aligns with responsible business guidelines issued by the Government of India.

| Regulation | Key Requirement | Deadline | Applicable To | Risk if Ignored |

|---|---|---|---|---|

| SEBI Listing Obligations and Disclosure Requirements (LODR) | Mandatory BRSR disclosure in Annual Report | Every Financial Year | Top 1,000 listed companies | Regulatory queries |

| National Guidelines on Responsible Business Conduct | Sustainability reporting principles | Continuous | Listed entities | Governance risk |

| SEBI BRSR Circular | Structured ESG disclosures | Annual | Listed companies | Compliance violation |

| Companies Act 2013 | Director accountability for disclosures | Annual | Public companies | Legal liability |

For listed companies, BRSR reporting is closely reviewed by:

Companies with incomplete ESG disclosures may experience:

Global institutional investors managing portfolios exceeding USD 30 trillion increasingly rely on structured ESG data when evaluating listed companies.

SEBI requires mandatory BRSR reporting from the largest publicly listed companies in India.

The reporting mandate applies to companies ranked within the top 1,000 listed entities by market capitalization.

These companies represent a substantial portion of India’s market value and economic activity.

Industries covered under mandatory BRSR reporting include:

Important thresholds and requirements include:

Companies ranked outside the top 1,000 may voluntarily submit BRSR disclosures to improve ESG transparency.

Voluntary BRSR adoption is increasing among mid-sized companies seeking improved access to global investment capital.

The BRSR reporting framework is divided into three primary sections designed to capture comprehensive ESG performance information.

Each section requires structured disclosures supported by numerical indicators and management commentary.

This section captures basic corporate information and business operations data.

Companies must provide details such as:

Typical metrics reported include:

This section provides investors with contextual information about the company’s operational scale.

This section focuses on corporate governance systems and sustainability management frameworks.

Companies must disclose internal policies, oversight mechanisms, and risk management structures used to monitor ESG performance.

Important disclosures include:

Companies also report governance metrics such as:

Large listed companies typically conduct 4–8 board meetings annually, with sustainability increasingly becoming a regular agenda item.

This section forms the core of BRSR reporting.

It measures corporate performance against the 9 principles of responsible business conduct.

| Principle | Disclosure Area |

|---|---|

| Principle 1 | Ethics and transparency |

| Principle 2 | Sustainable product lifecycle |

| Principle 3 | Employee well-being |

| Principle 4 | Stakeholder engagement |

| Principle 5 | Human rights protection |

| Principle 6 | Environmental sustainability |

| Principle 7 | Responsible policy advocacy |

| Principle 8 | Inclusive economic growth |

| Principle 9 | Consumer value protection |

Companies must provide numerical disclosures such as:

For example, large manufacturing companies may disclose:

These performance indicators allow investors to compare ESG performance across industries.

Environmental disclosure represents one of the most detailed components of the BRSR framework.

Companies must provide verifiable data related to resource consumption and environmental impact.

Key reporting categories include:

Companies must disclose:

Typical energy consumption reported by large industrial companies includes:

Companies must disclose:

Large industrial companies often report:

Waste reporting includes:

Typical waste disclosures may include:

The social pillar of BRSR reporting evaluates workforce management, safety standards, and employee welfare.

Companies must disclose detailed workforce data including:

Typical workforce disclosures include:

Safety indicators such as Lost Time Injury Frequency Rate (LTIFR) are also commonly reported.

Governance disclosures focus on ethical business conduct and corporate accountability.

Companies must disclose information related to board structure, compliance policies, and anti-corruption mechanisms.

Key governance disclosures include:

Typical governance structures in listed companies include:

| Step | Authority | Timeline | Documents Required | Risk Area |

|---|---|---|---|---|

| ESG data collection | Company ESG team | April–May | Sustainability data | Incomplete records |

| BRSR preparation | Compliance team | May–June | BRSR format | Data inconsistencies |

| Board approval | Board of directors | June–July | Annual report | Governance delay |

| Exchange filing | NSE / BSE | With annual report | Final BRSR | Regulatory queries |

Most companies require 6–10 weeks to collect ESG data from different departments including:

Early preparation reduces the risk of incomplete reporting.

Many companies face challenges when compiling sustainability data.

Common compliance risks include:

Operational data from factories may not match sustainability reports.

Collecting ESG data from hundreds of suppliers can be difficult.

Incorrect reporting of board independence or policy implementation can trigger regulatory queries.

Failure to properly submit BRSR disclosures may lead to several regulatory consequences.

Possible risks include:

Corporate directors may also face governance scrutiny under provisions of the Companies Act 2013.

BRSR reporting represents a significant shift in corporate disclosure practices in India.

Sustainability performance is no longer treated as optional corporate messaging. It has become a measurable compliance framework linked to investor confidence and governance standards.

Companies that build structured ESG reporting systems will find it significantly easier to comply with BRSR requirements.

Organizations that delay ESG data collection risk facing compliance challenges, regulatory scrutiny, and investor concerns.

Early preparation, accurate data tracking, and internal ESG governance mechanisms are essential for successful BRSR reporting.

📞 +91 78350 06182

📧 wecare@greenpermits.in