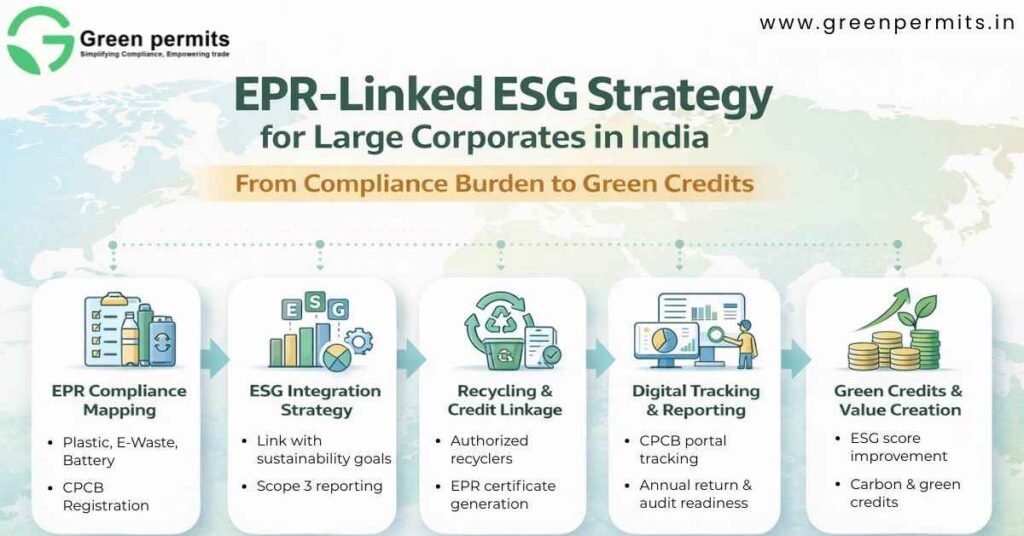

EPR-Linked ESG Strategy for Large Corporates in India 2026: From Compliance Burden to Green Credits

A leading FMCG company recently faced a CPCB compliance delay because its plastic packaging data on the EPR portal didn’t match its sustainability disclosures. What looked like a minor reporting issue quickly turned into a regulatory risk and ESG credibility concern.

This is no longer an isolated issue.

Across sectors like FMCG, electronics, automotive, and chemicals, companies are realizing that EPR compliance and ESG reporting must align at a data level—not just at a narrative level.

Why EPR is Now a Core ESG Lever for Large Corporates

EPR has evolved from a regulatory checkbox into a measurable sustainability metric that directly impacts ESG ratings, investor reporting, and operational continuity.

Today, regulators and investors expect data-backed sustainability, not declarations.

Key Shifts in Corporate Compliance Reality

EPR targets are now quantified and enforceable across sectors

ESG disclosures require auditable waste recovery data (MT basis)

CPCB portal acts as a central compliance ledger

Large corporates handling 10,000–1,00,000 MT waste annually must show traceability

Why This Matters for Corporates

ESG ratings now depend on actual recovery percentages, not policies

Investor due diligence increasingly includes regulatory compliance checks

Non-alignment between ESG reports and CPCB data can trigger:

audit flags

regulatory notices

reputational damage

For companies with ₹500 crore to ₹5,000 crore turnover, even a 5–10% compliance gap can translate into major ESG disclosure risks.

EPR Targets & ESG Measurement: Turning Waste into Measurable Metrics

EPR obligations are now structured in percentage-based targets, making them directly measurable and reportable under ESG frameworks.

Target Structure for Key Waste Streams

Minimum 8% recovery obligation in initial years

Increase to 13% in mid-phase compliance cycles

Scale up to 18% in long-term obligations

How Corporates Should Interpret These Numbers

For a company introducing 20,000 MT of plastic packaging annually:

8% target = 1,600 MT recycling obligation

13% target = 2,600 MT

18% target = 3,600 MT

These numbers directly feed into:

ESG sustainability metrics

circular economy performance indicators

Scope 3 emission reductions

ESG Impact Areas

Waste diversion from landfill (MT/year)

Resource recovery efficiency (%)

Recycled material usage (%)

Carbon reduction from secondary materials

Companies failing to quantify these metrics risk ESG score downgrades.

Regulatory Framework Governing EPR-Linked ESG

Regulation

Key Requirement

Deadline

Applicable To

Risk if Ignored

Plastic Waste Rules (Amended)

Category-wise EPR targets

30 June annual filing

Brand Owners, Importers

Portal suspension

Battery Waste Rules

Collection & recycling obligation

Annual cycle

Manufacturers, Importers

Environmental compensation

ELV Rules

Certificate purchase obligation

30 April declaration

Automobile sector

Registration rejection

Environment Protection Act

Legal enforcement

Continuous

All entities

Fine + imprisonment

Business Interpretation

Compliance is now multi-regulatory, not single-rule

One company may fall under 2–4 EPR categories simultaneously

Non-compliance in one category can impact overall ESG credibility

How CPCB Portal Drives ESG Accountability

The CPCB portal is no longer just a filing system—it is a real-time compliance tracking mechanism.

Core Functions That Impact Corporates

Digital registration of producers and importers

Certificate generation and transaction tracking

Quarterly data validation

Annual audit-ready reporting

Compliance Data That Must Match ESG Reports

Quantity introduced in market (MT)

Quantity recycled (MT)

Certificates purchased (units/MT)

Shortfall (if any)

Typical Compliance Timelines

Step

Timeline

Risk Level

Registration approval

15–30 days

Medium

Target declaration

Before 30 April

High

Certificate procurement

Ongoing

High

Annual filing

Before 30 June

Critical

Practical Risk

Even a 2–3 week delay in certificate procurement can result in:

filing rejection

carry-forward liability

ESG reporting mismatch

EPR Certificates as ESG Assets: The Green Credit Opportunity

EPR certificates are emerging as measurable sustainability instruments that corporates can strategically manage.

How the Model Works

Recyclers process waste and generate certificates (per MT)

Producers purchase certificates to meet obligations